Real Property Gains Tax (RPGT) Guide for the Year 2020-2021 in Malaysia

*This article was updated on 15 June 2021.

Thanks to the new incentives announced during PENJANA 2020, Malaysians who sell off their residential property between 1 June 2020 and 31 December 2021 will be exempted from paying the 5% or higher RPGT for the disposal of properties.

RPGT 2020 Exemptions

In light of the Covid-19 outbreak, Prime Minister Tan Sri Muhyiddin Yassin introduced several incentives during the PENJANA briefing on 5 June to help boost the property market and provide financial relief to homebuyers and homeowners. These include the reintroduction of the HOC 2020 (Home Ownership Campaign) which features stamp duty exemptions as well as special RPGT 2020 exemptions. Malaysians will be exempted from paying the 5% (or higher) RPGT for the disposal of residential property from 1 June 2020 and 31 December 2021. The exemption is limited to the disposal of three units of residential homes per individual.

That aside, both local and foreign homeowners, as well as companies, would need to equip themselves with the basic know-how of RPGT, especially on how to calculate the applicable RPGT rates and what are the available exemptions for each of them.

Following is what you need to know.

What is Real Property Gain Tax (RPGT) Malaysia?

According to the Real Property Gains Tax Act 1976, RPGT is a form of Capital Gains Tax in Malaysia levied by the Inland Revenue (LHDN). It is chargeable upon profit made from the sale of your land or real property, where the resale price is higher than the purchase price.

RPGT is generally classified into 3 tiers:

Individuals (Citizens & Permanent Residents)

Individuals (Non-Citizens/Foreigners)

Companies

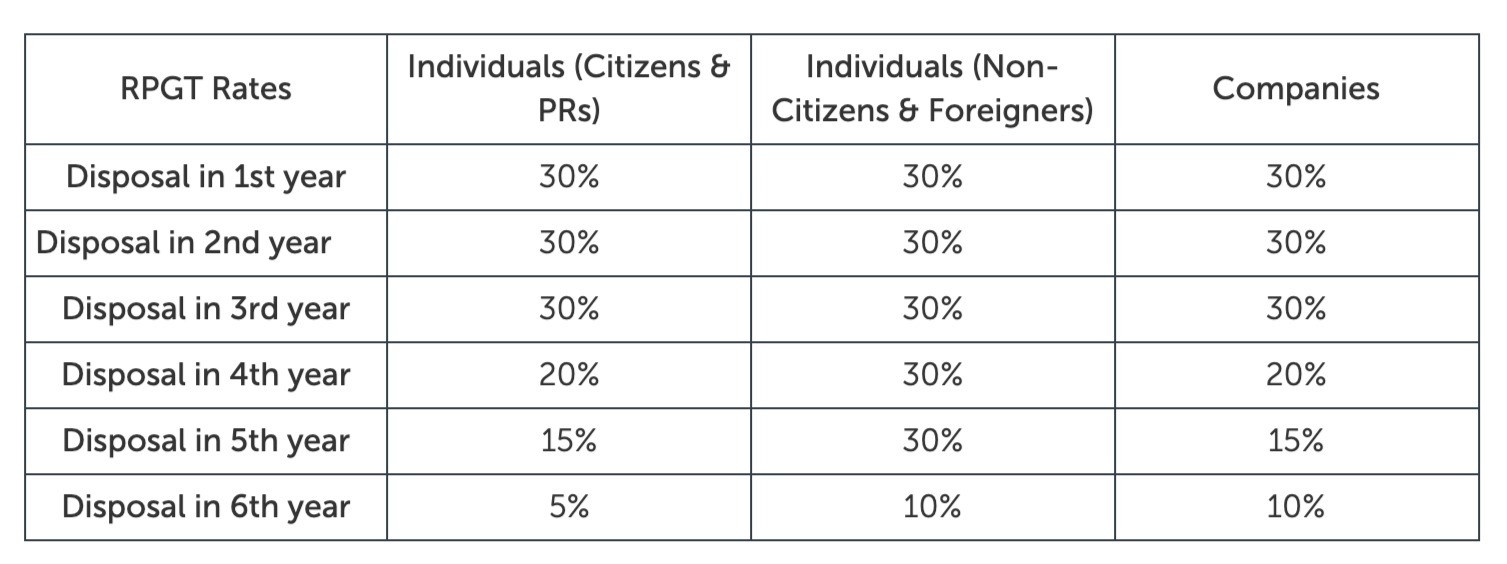

It was first implemented in 1995 and it has seen quite a few changes over the years. The most recent RPGT amendment which was announced during Budget 2019 and implemented in January 2019 was the seventh one so far – where Malaysians who are selling off their property in the sixth (and subsequent) years of ownership will now have to pay a 5% RPGT. Foreigners and companies will also see an increase in RPGT rates, from 5% to 10%.

Previously, Malaysian homeowners who sell off their properties after the 5th year of ownership are not required to pay any RPGT on the profits earned from the sale. Meanwhile, companies and foreign homeowners were required to fork out 5% for RPGT.

How much is RPGT in Malaysia?

New RPGT Rates from January 2019

As you can see from the above, RPGT rates from the 6th year onwards have increased to twice the existing rates for all the 3 tiers.

Who should pay RPGT?

RPGT is not applicable if the disposal price of a property is deemed equal to or lower than the acquisition price. It is only chargeable if there is a profit gain from the disposal of the real property.

1. Individuals (Citizens, PRs, Non-Citizens & Foreigners)

If any of the above parties sell their property at a profit, they will have to pay RPGT based on their chargeable gain.

2. Companies

Usually, the selling of shares by companies are not subject to RPGT except Real Property Companies (RPCs) whose core business is in real property. An RPC company constitutes only if it has real property or RPC shares amounting to no less than 75% of its company’s total tangible assets. However, if the company disposes of its shares or real property to the point where its RPC share percentage falls below 75% and it ceases to be an RPC, then the shares that are disposed of will not retain their RPC characteristic and will be liable for the RPGT provision.

Additionally, if a company reclassifies its real property from fixed asset to current asset (say, trading stocks) then it is also deemed as a disposal of a chargeable asset and is subject to RPGT. The disposal price of such assets will be at their market value at the date of reclassification.

NOTE: A property development company will be regarded as an RPC as real property includes the development land situated in Malaysia. This is notwithstanding that the development land itself is subject to income tax and not RPGT.

RPGT 2020 exemptions for Individuals & Companies

RPGT Exemptions for Individuals in 2020

1) An exemption of 10% of profits or RM10,000 per transaction (whichever is higher) for the following four scenarios:

Malaysian citizens & Permanent Residents

a) If an asset is transferred as a gift by a donor who is a Malaysian citizen and the acquirers are either husband and wife, parent and children or grandparents and grandchildren. This exemption is not applicable for transfers between siblings.

b) Once in a lifetime exemption on the chargeable gain on disposal of 1 private residence by a Malaysian citizen or

Non-Citizens & Foreigners

c) If an asset is transferred between spouses, then the asset to be disposed of must be owned by the husband or wife who is a Malaysian citizen.

d) If an asset is transferred to a company, then the asset owner or owner’s spouse must be a Malaysian citizen. If the asset is jointly owned by 2 individuals, both need to be Malaysian citizens to make the transfer.

2) Homeowners who own low or medium cost housing priced below RM200,000 are exempted from RPGT when disposing of their property.

RPGT Exemptions for Companies

1) 10% of profits or RM10,000 per transaction (whichever is higher) is exempted

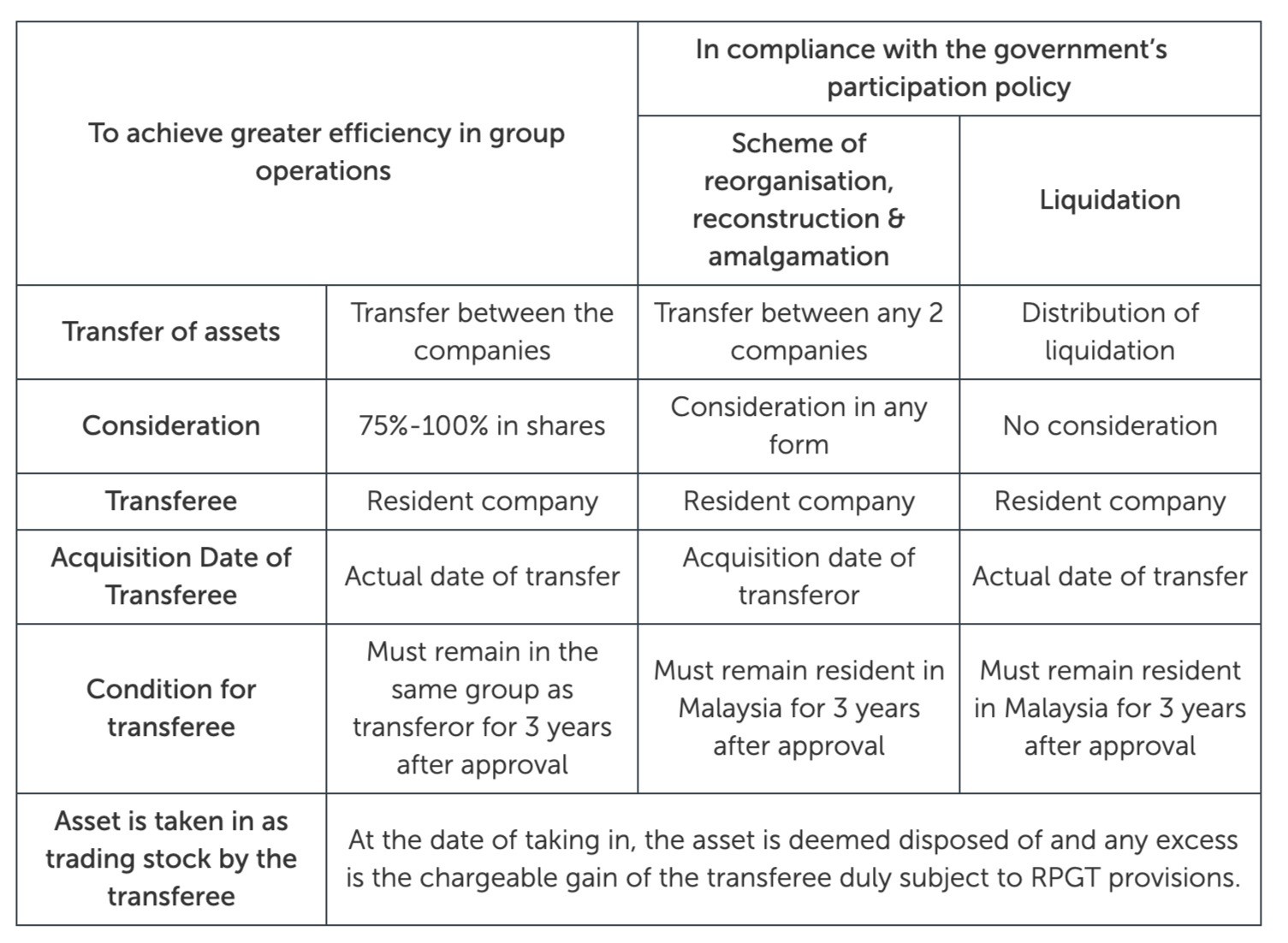

2) Intercompany transfer of shares is exempted from RPGT as follows:

Allowable Expenses for RPGT

Any incidental costs incurred in disposing of the property (as follows) can be deducted from chargeable gain to calculate RPGT:

Legal fees, accounting fees, surveyor’s fee, etc.

Real estate fees (sales commission)

Administrative fees

Repair or renovation to maintain or upgrade the property such as interior design

Cost of preserving or defending one’s title to, or to a right over the asset

Cost of advertising to make the disposal

What is Allowable Loss for RPGT?

If there is more than one transaction of real property in the assessment year, any loss incurred from a single transaction can be offset against another transaction, which generates a chargeable gain, as long as both the transactions fall under the same year.

How do I determine the applicable RPGT years?

1) The property acquisition and disposal dates are based on the date of signing the Sales and Purchase Agreement (SPA) for both completed and under-construction properties.

2) Say you inherited a property from a relative or friend who has passed away, when selling it off (you will be known as the executor), as per the RPGT Act for deceased’s estates:

Date of death of the deceased = Acquisition Date by the executor

The executor oversees the selling or disposing of the estate before distributing it to the beneficiaries. The RPGT charged on the deceased person’s estate is based on this acquisition date by the executor.

RPGT amendment under Budget 2020

In last year’s Budget 2020 tabling, an RPGT amendment was made to provide some relief to property sellers – it was announced that for the calculation of property gain tax of units purchased before 2013, the Government will use the market price on 1st January 2013 as the initial point of valuation. Previously, the base year was set at 1 January 2000. As RPGT is charged on the profit made from the sale, a later base rate would mean a lower calculated profit, thus reducing the property seller’s tax burden.

How to calculate RPGT in Malaysia?

RPGT Calculation For Individuals

The following formulas are the same for Citizens, PRs, Non-Citizens & Foreigners. Their RPGT rates will vary depending on their holding period and residential status (refer to the table above).

RPGT is charged on Net Chargeable Gains.

Gross Chargeable Gain: Acquisition price – Disposal priceNet Chargeable Gain: Gross Chargeable Gain – Allowable Expense – RPGT Exemption – Allowable LossTAX PAYABLE = RPGT Rate (based on the number of years of property ownership) X Net Chargeable Gains

Example: For instance, let’s say Adam and Hanis (both Malaysian citizens) bought a condominium in Hartamas on 4th January 2013 for RM300,000. With plans to start a family, they decided to upgrade to a bigger place and on 20, January 2019 they sold off the condominium for RM500,000.

Gross Chargeable Gain: RM 500,000 – RM 300,000 = RM 200,000

Assuming Adam has an Allowable Expense of RM 30,000 and an RM20,000 RPGT Exemption of 10% of profit (200,000 x 10%)*

Net Chargeable Gain: RM 200,000 – RM 30,000 – RM 20,000 = RM 150,000

TAX PAYABLE = 5% RPGT x RM 150,000 = RM 7,500.

(RPGT rate is based on Budget 2019 for Individual Citizens disposal in 5th years as the property holding period is 5 years)

RPGT Calculation For Companies

Acquisition Price: A/B x C, where A = number of shares held by the shareholder; B = total issued shares of the companyC = the defined value of the real property at the date of acquisition of the chargeable asset

Gross Chargeable Gain: Disposal Price – Acquisition PriceNet chargeable Gain: Gross Chargeable Gain – Allowable Expense – RPGT Exemption –Allowable LossTAX PAYABLE = RPGT Rate (based on the number of years of property ownership) x Net Chargeable Gains

Example:

Synergy Sdn Bhd was incorporated on 1 January 2013 with Mr Andrews, Mr Brian & Mr Tate holding 100,000 shares each. It was not an RPC during the time of its incorporation. However, on 31st March 2015, the company acquired its first and only real property at RM 1.2 million. As a result, its total tangible assets including the real property became RM 1.5 million, turning it into an RPC.

On 31, January 2019, Mr Andrews decided to sell his 100,000 shares for RM 1 million to Mr Lodge.

Acquisition Price: 100,000/300,000 x RM 1,200,000 = RM 400,000Disposal Price: RM 1,000,000Gross Chargeable Gain: RM 1,000,000 – RM 400,000 = RM 600,000Assuming Mr Andrews have Allowable Expense of RM 50,000, an RPGT Exemption of RM 600,00 ( *600,000 x 10%) and Allowable Loss of RM 35,000.Net Chargeable Gain:** RM 600,000 – RM 50,000 – RM 60,000 – RM 35,000 = RM 455,000

TAX PAYABLE = 30% RPGT X RM 455,000 = RM 136,500

(RPGT rate is based on Budget 2019 for Companies disposal in the 3rd year as the property holding period is 3 years)

When do you have to pay RPGT in Malaysia?

For locals and permanent residents who sell off a property, their lawyers will retain 3% of the property’s selling price/disposal price when the purchaser pays the first deposit to buy the property for the purpose of RPGT payment. For non-citizens & foreigners, this retention rate is 7%.

Your solicitor will make the payment with necessary forms to Inland Revenue Board within sixty (60) days from the date of the sale and purchase agreement to meet the RPGT payable.

How to file RPGT in Malaysia?

Those who wish to file their RPGT themselves can obtain the necessary forms from the nearest LHDN branch or download them from IRB’s website.

STEP 1: Complete the Disposal of Real Property (CKHT 1A) form, your Sales and Purchase Agreement (SPA) form and other documents supporting the RPGT deductions you plan to make.

STEP 2: Fill out the Notification under Section 27 in the RPGTA 1976 (CKHT 3) form – to apply for RPGT exemptions.

STEP 3: Get your property purchaser to complete the Acquisition of Real Property (CKHT 4) form that usually comes hand in hand with a copy of the SPA.

STEP 4: Submit all forms and supporting documents to the nearest LHDN branch within 60 days of the sale.

What is the consequence of late payment of RPGT?

Any payment after 60 days may attract a penalty payable by the seller. The penalty is 10% of the amount payable as RPGT.

This article has been repurposed and first appeared in iProperty

Penafian

Kandungan yang disediakan di laman web ini adalah bertujuan untuk maklumat am dan tujuan pendidikan sahaja. Ia tidak membentuk nasihat undang-undang, dan tidak seharusnya diandalkan sebagai pengganti rundingan profesional dengan peguam yang berkelayakan. Setiap kes undang-undang adalah unik, dan anda amat digalakkan untuk mendapatkan nasihat undang-undang khusus daripada pengamal undang-undang berlesen sebelum mengambil sebarang tindakan berdasarkan maklumat yang terdapat di sini.

Walaupun kami berusaha untuk memastikan ketepatan dan kemas kini kandungan tersebut, ASCOLAW dan sekutunya tidak membuat sebarang representasi atau jaminan dalam apa jua bentuk, sama ada secara nyata atau tersirat, tentang kelengkapan, ketepatan, kebolehpercayaan, kesesuaian atau ketersediaan maklumat yang terkandung di laman web ini. Sebarang keandalan yang anda letakkan pada maklumat tersebut adalah atas risiko anda sendiri sepenuhnya.

Bidang Amalan

Artikel Berkaitan

Terma dan Syarat Perlantikan Peguam

Cara Pindah Milik Rumah Selepas Cerai di Malaysia

5 Situasi Pemilik Bersama Tanah Perlukan Perintah Mahkamah di Malaysia

Debt Recovery Process in Malaysia (Proses Tuntut Hutang)

Love and Affection Transfer: Process of Giving Land or House Title to Children in 2025

Peguam Hartanah di Malaysia

Surat Kuasa Mentadbir di Malaysia

Guide to Appointing a Property Lawyer and the Cost of Fees for House and Land Purchase Transactions in 2025

Real Estate Lawyer In Malaysia

Simple Guide to Changing the Name on a Land and House Title After a Death